Jump To:

Saving Social Security: Which Solutions Do Americans Support?

According to the 2025 Trustees Report estimates, Social Security will only have sufficient funds to pay full benefits until 2033. After that, payroll tax and other revenues would cover only 81% of benefits. However, this financing gap can be closed if lawmakers act on proposed solutions.

A bipartisan survey found that across party lines, generations, and income and education levels, Americans want lawmakers to strengthen Social Security's finances by increasing program revenues rather than cutting benefits. When asked about their views, 85% of those surveyed responded that benefits should not be reduced, or benefits should be increased, even if that meant raising taxes on some or all Americans. Here are a few key solutions that respondents weighed in on.

Sources: Social Security Administration, 2025; National Academy of Social Insurance, January 2025

Navigating Financial Conversations with Aging Parents

Having a conversation with your parents about their finances can seem like a daunting task. However, it is an essential step in helping to ensure their financial well-being as they get older. Here are some practical tips to help you navigate these discussions.

Start the conversation

Talking about money can be difficult. However, it's important to initiate a financial conversation with your parents before they become too ill or incapacitated. Your parents may be unwilling to talk to you at first because they are reluctant to give up control over their financial affairs, or they are embarrassed to admit that they need your help. It's important to approach the topic sensitively and make it clear that you fully respect their needs and concerns.

If they are still hesitant to talk to you and are capable of managing their affairs for now, you may want to revisit the discussion later. Or you could suggest that they talk to another family member, trusted friend, attorney, or financial professional.

Organize financial and legal documents

Once the lines of communication are open, you can help your parents organize their financial and legal documents. Start by creating a personal data record that lists the following types of information:

Financial: Include all of your parents' bank/investment account information, including account/routing numbers and online usernames and passwords. You should also list any real estate holdings, along with any outstanding mortgages. Do your parents receive income from Social Security, a pension, and/or a retirement plan? You will want to include that information as well.

Legal: Find out if your parents have had any legal documents drawn up, such as wills, trusts, durable powers of attorney and/or health-care directives. Locate other important documents too, such as birth certificates, property deeds, and certificates of title.

Medical: Determine what type of health insurance your parents have — Medicare, private insurance, or both. You should also have the names and contact information for their health-care providers, their medical history, and any current medications.

Insurance: List what other types of insurance coverage your parents have — life, home/property, auto, or long-term care, for example — along with the names of their insurance companies and policy numbers.

Store the data record and any other pertinent documents either electronically or in a secure, fireproof box or file cabinet.

Who Are Caregivers Caring For?

Source: SeniorLiving.org, 2025

Help with managing finances

You can help your parents manage their finances by examining their budget and finding out their monthly income and expenses. Track your parents' spending to make sure that they are living within their means. You should also discuss ways to address any outstanding debts they may have.

Find out how your parents pay their bills and expenses. If they still use traditional methods, encourage them to set up safer and more convenient ways to bank such as direct deposit and making payments online, instead of mailing paper checks. If your parents are uncomfortable with electronic payments, remind them to mail all bills inside the physical post office and not to use outdoor mailboxes, which may be targets for mail theft.

Do your parents need additional support in managing their finances? There are ways for you to obtain the necessary authorization to assist them. One way is to become a joint account holder on certain bank accounts. This can give you direct access to manage transactions, monitor account activity, and ensure bills are paid. However, being a joint account holder may have certain legal and tax ramifications. Another option is for them to obtain a durable power of attorney, which is a legal document that grants you authorization to make financial decisions on their behalf, even if they become incapacitated. It may also be helpful for them to add you or someone else as a trusted contact for their accounts.

Discuss estate planning issues

If they haven't already done so, make sure your parents have certain legal documents in place — such as wills and/or trusts — to ensure that their estate planning wishes are followed. In addition, they may need to have a durable power of attorney, health-care proxy, and living will in place so they have someone to manage their money and health-care issues if they become ill/impaired. Issues surrounding the care of an aging parent can be complex. Consider consulting a financial professional and/or elder law attorney who specializes in financial and legal issues that affect older adults.

Avoiding Probate with a TOD Deed and TOD Account

If you want to leave your home to your children or other heirs and keep the property out of the costly and time-consuming probate process, you could place your home in a living trust. Trusts offer numerous advantages, but they incur up-front costs, often have ongoing administrative fees, and involve a complex web of tax rules and regulations.

More than half of U.S. states offer a simpler and less expensive way to avoid probate through a transfer-on-death (TOD) deed (also called a beneficiary deed). As the name suggests, this is a legal document that directly transfers ownership of the property from you to your designated beneficiary or beneficiaries upon your death. You retain full ownership and control while you are alive, and your beneficiary has no rights to the property until after your death. (Beneficiaries also inherit any associated financial obligations, such as a mortgage or lien.)

The TOD deed must be filed with the appropriate land records office. The deed supersedes your will, so be sure the provisions of your will match the deed. If you change your mind, the deed can be revoked and/or replaced through a new filing. As with all beneficiary documents, it would be wise to designate contingent beneficiaries in the event that a designated beneficiary predeceases you.

In some states, a married couple who own a house together through joint tenancy or as community property with right of survivorship would each have to complete a TOD deed. The deed for the first spouse who dies would be void, and the deed for the second spouse would transfer ownership to the designated beneficiary(ies).

TOD accounts

In most states, you can apply a transfer-on-death provision to individual non-retirement brokerage accounts. This typically involves filing a form with the financial institution to designate a beneficiary or beneficiaries (including contingent beneficiaries) and register the account as TOD. Ownership of the TOD account would transfer directly to the designated beneficiary(ies) upon your death without going through probate. Like TOD deeds, a TOD account designation supersedes your will.

For a joint account, the effect of a TOD designation would depend on the type of account.* Retirement accounts generally go directly to the beneficiary(ies) without probate and do not require being retitled as TOD.

Bank accounts offer a similar designation called Payable on Death (POD). One key difference is that POD accounts typically do not allow contingent beneficiaries.

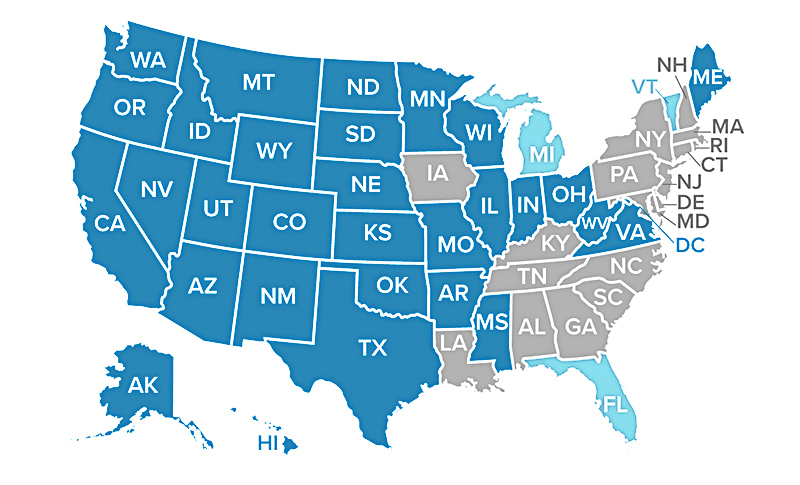

States in dark blue allow a TOD deed

Florida, Michigan, and Vermont (light blue) allow a similar document called an enhanced life estate deed or Lady Bird deed. Texas and West Virginia allow TOD and Lady Bird deeds. Source: Nolo, October 8, 2024

Estate and capital gains taxes

A TOD deed or account designation does not remove the property or account assets from your taxable estate. However, with high federal estate tax exclusion amounts, few estates would likely be subject to federal estate taxes.**

If your heirs sell your home or account assets, they could be subject to capital gains taxes regardless of whether they receive the property/account through a living trust or a TOD deed. However, the step-up in basis provision of U.S. tax law automatically sets the basis as the fair market value of the home or account at the time of your death, effectively eliminating all capital gains up to that time. Your heirs could shelter $250,000 of gains ($500,000 for a married couple) if they live in the home for two out of five years before selling. (There is no shelter provision for financial accounts.)

Although you do not need an attorney to execute a TOD deed in most states, you may want to consult an attorney familiar with the laws of your state. You should consider the counsel of experienced estate planning, legal, and tax professionals before implementing trust strategies.

*A TOD designation on a joint ownership/tenancy or tenants by/in the entirety account would only become effective if both owners die simultaneously. A TOD on a tenants in common account would be similar to an individual account.

**For estates of those who die in 2025, the exclusion is $13.99 million, with a combined $27.98 million exclusion for a married couple.

Concerned About Cyberattacks? The Threat Is Real

According to a 2024 survey, 60% of small businesses believe that cyberattacks are the biggest threat they currently face, and rightly so.1

When a data breach occurs, hackers gain access to the personally identifiable information of customers or other individuals, opening the door for identity theft and other financial crimes. Even small companies can be held legally responsible when their customers' personally identifiable information is disclosed. Moreover, the time and expense involved in recovering from any type of cyberattack could be insurmountable.

Does your company handle potentially sensitive information about customers, employees, or competitors? If so, you may want to be proactive about addressing this risk.

Methods of attack

Phishing often involves emails sent to employees. Clicking on a link provides access to the company's network, allowing the installation of malicious code (malware) designed to steal or hijack critical data.

A watering hole attack targets individuals or organizations by infecting websites that they frequently visit with malware.

Ransomware is a menacing virus that locks businesses out of their computer files and demands payment of a ransom in exchange for the return of company systems and data.

Fortify your defenses

The Federal Communications Commission has some cybersecurity tips for small businesses.

- Install and update antivirus software on every computer, and maintain firewalls between the internal network and the Internet. Lock up computers, laptops, and tablets to prevent them from falling into the wrong hands.

- If you have a Wi-Fi network, set it up so the network name is hidden and a secure password is required for access. Require passwords to be changed on a regular basis.

- Train employees in security practices, especially not to open emails from unknown senders. Set up a separate account for each user, and provide access only to the data needed for users to perform their jobs. Backup critical data regularly and delete data when it's no longer needed.

- Consider purchasing cyber insurance, which may offer some protection (up to policy limits) from the financial repercussions of a cyberattack, such as the cost of restoring lost or stolen data; liability stemming from a security failure; and in some cases, lost income due to business interruption.

The cost of cyber insurance depends on the types of coverage selected, and policies have exclusions, terms, and conditions for keeping them in force.

1) U.S. Chamber of Commerce, 2024